July 13, 2026

July 13, 2026

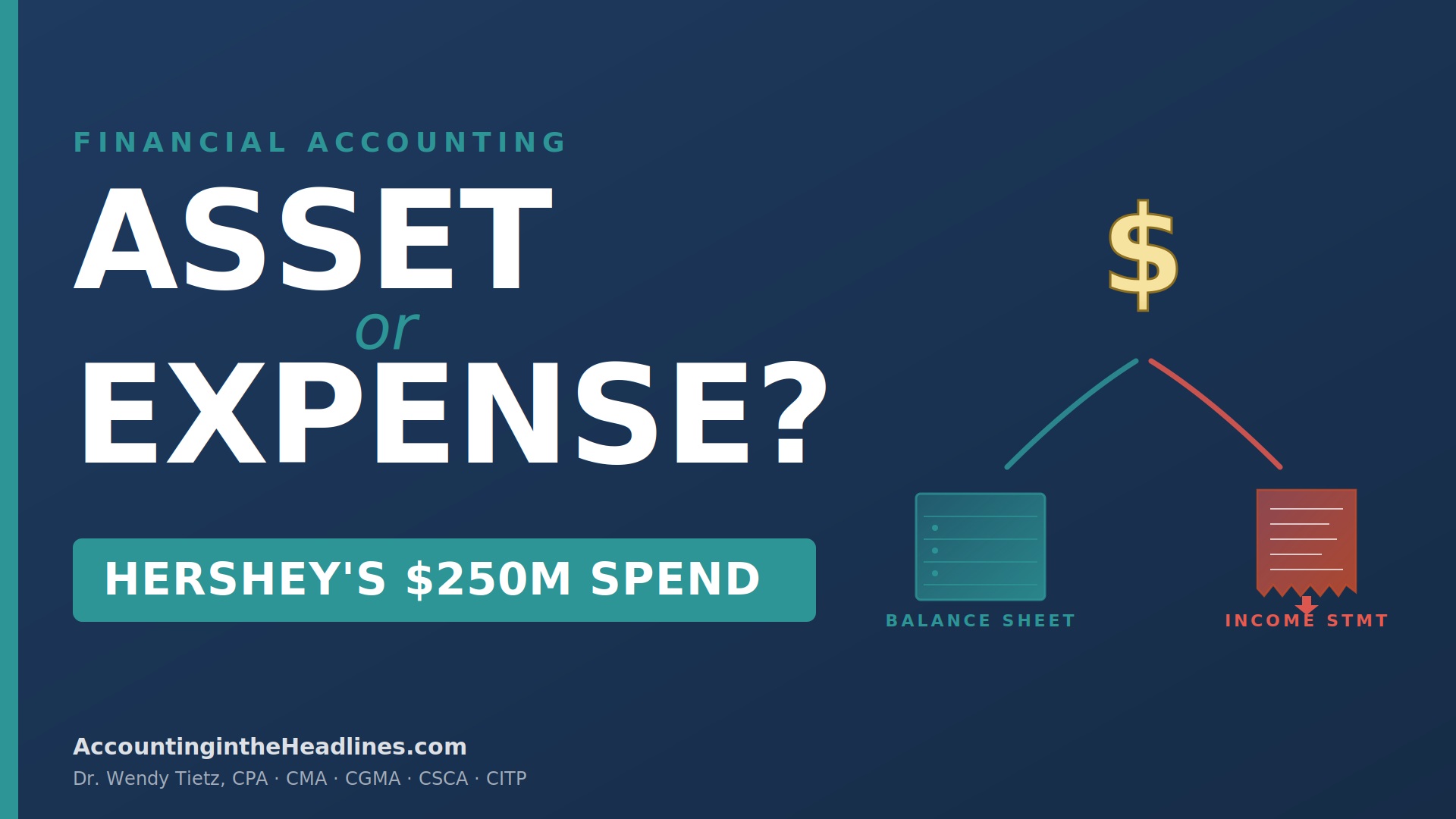

The Hershey Company (NYSE: HSY), a well-known confectionery and salty snack maker, is spending significant amounts on technology across its supply chain. At Hershey’s 2026 Investor Day held in late March 2026, Hershey’s chief supply chain officer, Jason Reiman, highlighted a $250 million supply chain and manufacturing initiative originally launched in 2024 that focused on digitizing processes, improving visibility, streamlining operations, and optimizing procurement and manufacturing.

A project of this size includes many different categories of cost: software licenses and platforms, computer hardware and servers, factory-floor sensors and equipment, installation and testing, employee training, consulting and professional services, and ongoing information technology support. Not all of these costs are treated the same way on Hershey’s financial statements.

Under U.S. GAAP, costs that provide probable future economic benefit to the company beyond the current period and that can be measured reliably are generally capitalized as assets (either as property, plant, and equipment or as intangible assets) and then expensed over time through depreciation or amortization. Costs that do not create a separately identifiable, controllable asset, or that relate only to the current period, are generally expensed as incurred.

For Hershey’s supply chain project, that means a cost like the purchase of a software platform, the computer servers it runs on, or the factory sensors installed on the production floor would generally be capitalized. The installation, configuration, and testing work required to bring those assets into working condition would typically be capitalized as well. But costs like employee training on the new system, ongoing IT helpdesk support, and routine consulting relating to current operations would generally be expensed in the period incurred.

The classification matters because it directly affects the timing of the expense on the income statement, the size of the assets reported on the balance sheet, and the pattern of net income over time.

View a quick tutorial video about distinguishing capital expenditures from immediate expenses at this [link] and then answer the following questions.

Note to instructors: This post is assignable in Pearson’s MyLab and has questions that are auto-graded.

Discussion Questions

- Hershey’s $250 million supply chain project includes many categories of cost. Which types of costs would typically be capitalized, and which would typically be expensed as incurred? Give at least one example of each.

- How does the decision to capitalize versus expense a cost affect the balance sheet and the income statement in the year of the project?

- Employee training and certain consulting costs related to the rollout of new supply chain technology are generally expensed, even though they arguably provide benefits in future years. Why do you think U.S. GAAP treats those costs differently from the software and hardware themselves?

- If Hershey’s management were to classify more of its supply chain project costs as capital expenditures rather than period expenses, how would that choice affect Hershey’s net income in the year of the project and in future years? Why does this matter to financial statement users?

- Why do auditors and financial analysts pay close attention to how a company classifies technology project costs between capital expenditures and immediate expenses?

No comments yet... Be the first to leave a reply!